I. Introduction

It is evident that administrative activity must be oriented towards the general interest, guaranteeing predictability, coherence and full subjection to the principle of legality in the exercise of public powers, regardless of the level or administrative structure involved.

This general interest, which constitutes the very purpose of administrative action, imposes on officials the duty to exercise their powers effectively, efficiently, and expeditiously. In customs terms, this means implementing due control over foreign trade operations in the shortest time compatible with their purpose, avoiding delays that affect the dynamics of legitimate international trade.

No one disputes that Customs must exercise rigorous border control. This is their essential function: to monitor the entry and exit of goods, verifying compliance with the regime of prohibitions and restrictions, both economic and non-economic, as well as the tax regime applicable to foreign trade. Ultimately, this is a typical manifestation of the state's police power in economic and security matters.

However, it is essential that this control does not delay shipments longer than strictly necessary, since delays generate costs and these represent a loss of competitiveness. Therefore, it is the responsibility of Customs to collaborate in facilitating international trade. (1)

At the Singapore Ministerial Conference held in December 1996, the concept of trade facilitation was introduced for the first time into the official language of the World Trade Organization (WTO), understood as the process of simplifying and harmonizing international trade procedures. That is, the practices and formalities that refer to the collection, presentation, communication and processing of data necessary for the movement of goods in international trade. (2)

Obstacles to this process include excessive or redundant documentary requirements, investigations lacking technical support, disproportionate audits, lack of procedural transparency, lengthy and complex procedures, absence of controls based on risk assessment techniques, as well as insufficient technological modernization and deficient inter-institutional coordination, among other practices that compromise the efficiency of the system and whose enumeration is not intended to be exhaustive.

The antithesis of facilitation lies precisely in overregulation and excessive bureaucratization of customs procedures, which generate unnecessary delays and, simultaneously, erode the legal certainty of operators. In this necessary balance between control and facilitation, the concept of [the following] becomes especially relevant. intelligent control. Purely random control will continue to exist, but it is gradually giving way to selectivity schemes based on predefined risk profiles and patterns, which allow the focus of oversight activity on sensitive operations, without hindering the regular flow of legitimate trade.

Furthermore, interaction between different customs administrations is becoming increasingly important. Cooperation and mutual assistance agreements, alerts issued by the customs authorities of the country of origin or provenance of the goods, and early warning mechanisms make it possible to anticipate analysis and intelligence tasks, strengthening the effectiveness of controls and optimizing resource allocation.

Certainly, customs administrations around the world face significant challenges in the 21st-century global scenario, characterized by a process of globalization that has driven unprecedented international economic development and an ever-increasing integration of logistics chains.

There is an increasingly widespread demand for processes "just in time" which require increasingly shorter border crossing times. This is compounded by the greater complexity of international trade, stemming from liberalization processes that have led to sophisticated regulatory frameworks and the proliferation of regional and multilateral agreements.

Furthermore, this scenario of commercial expansion must be analyzed in light of a more complex world, where in addition to the so-called "tariff war", the problems of international terrorism, transnational organized crime, drug trafficking, human trafficking and international fraud have intensified, all of them capable of using the logistical circuits of international trade for their realization.

All of this has raised awareness in society regarding the strategic role of Customs. as key players in economic development and, at the same time, as guardians of the national border.

The challenge for modern Customs is therefore particularly complex, as it must rigorously control the entry and exit of goods in the face of systemic risks inherent in the contemporary international scenario and, simultaneously, perform its function as a facilitator of international trade, allowing operators to optimize costs and improve their competitiveness in the global arena.

In the specific area of facilitation, it is worth noting that, in June 2005, the World Customs Organization (WCO) developed the regulatory framework to secure and facilitate global trade, an instrument that establishes principles and minimum standards of action for adoption by member states.

The four basic elements of the WCO regulatory framework are: a) harmonisation of requirements for electronic advance information; b) consistency and common patterns in risk analysis to address security issues; c) interaction between customs administrations, inspection at origin against the reasonable request of the country of destination, in high-risk cases; and d) determination of advantages for actors who comply with minimum security standards.

The regulatory framework for facilitation is structured around two fundamental pillars of understanding. The first is the strengthening of relations between customs administrations and the genuine exchange of information. The second is the appropriate and ongoing relationship between customs administrations and the private sector.

Regarding relations between customs administrations worldwide, one of the fundamental aspects is the advance exchange of information. To this end, the WCO considers the electronic exchange of information advisable, and therefore, systems should be based on harmonized, interoperable messages.

To ensure effective control without hindering the smooth flow of goods, customs administrations must employ modern technologies when inspecting high-risk shipments, including high-powered X-ray and gamma-ray equipment and radiological detection devices. The use of these technologies to preserve the integrity of the cargo and containers is another essential element of this pillar.

2The Facilitation Agreement

The Trade Facilitation Agreement is the first multilateral trade agreement concluded since the creation of the World Trade Organization (WTO). It was adopted at the Ninth WTO Ministerial Conference, held in Bali, Indonesia, in December 2013.

At the dawn of the creation of the World Trade Organization, after the conclusion of the Uruguay Round and the signing of the Final Act in 1994, several member states began to outline the agenda for a new round of multilateral negotiations, identifying trade facilitation as one of its strategic axes.

As anticipated, the issue began to take shape at the 1996 Singapore Ministerial Conference. At this conference, "facilitation" was definitively established as a structural feature of modern customs activity. Since then, its impact has been measured. performance Customs, depending on the time taken to lift or clear the loads.

Subsequently, WTO members agreed to incorporate trade facilitation into the Doha Round work program for Development, and in 2004, the Negotiating Group on Trade Facilitation was formally established. The Agreement reached in Bali at the end of 2013 provides a framework of rights and obligations that tend to improve border procedures with the aim of reducing time and costs, strengthening the competitiveness of both States and economic operators.

In the Republic of Argentina, this Facilitation Agreement has been approved by the National Congress, through Law 27.373. The importance of the Agreement is quite evident, as it introduces the definition of best practices for customs processes into the agendas of customs administrations worldwide.

World Bank statistics are telling: countries with higher levels of administrative efficiency are the most competitive, and trade facilitation aims to create streamlined and efficient customs processes, thereby reducing direct and indirect costs associated with international trade, increasing the competitiveness of businesses, and thus improving their performance. performance, which in turn will generate greater economic growth.

Expert opinion has highlighted that forty percent (40%) of cross-border costs are due to procedural inefficiencies, such as delays in customs clearance, excessive documentation requirements, and, repeatedly, cumbersome documentation requirements and unnecessary inspections, among other issues. (3) In this sense, the Agreement constitutes an institutional response to such inefficiencies, aimed at adopting common policies designed to reduce time and costs.

It is instructive to recall the words of Pascal Lamy, then Director-General of the WTO, when speaking on this topic at the Chittagong Chamber of Commerce in Bangladesh in 2013, on which occasion he pointed out that “Multilateral trade negotiations are sometimes difficult to relate to the day-to-day work of trade operations. But this is not the case with trade facilitation. Effective trade facilitation increases customs productivity, improves tax collection at borders and helps attract foreign direct investment. A multilateral agreement on trade facilitation could speed up the cross-border movement of goods and improve the transparency and predictability of trade and business operations.”

In conceptual terms, facilitation aims to simplify, standardize, harmonize, and automate the procedures applied to international trade, with the purpose of streamlining the movement, release, and dispatch of goods.

This involves generating efficient, effective and agile procedures, so that the loads take the minimum time necessary for proper control to be carried out, depending on the circumstances of the operation, in order to reduce direct and indirect costs associated with international trade. This is the objective of facilitation, to reduce time and costs.

This is certainly a cultural change, a paradigm shift, because historically, in many cases, customs administrations have not taken into account the "time" factor as a relevant variable in their auditing tasks.

Among the main obstacles identified are the existence of complex and imprecise operating procedures, lacking clear deadlines and not being auditable in real time. Such schemes create margins of discretion that are incompatible with the logic of facilitation.

Furthermore, the requirement for excessive or repetitive documentation is a significant source of inefficiency. Several World Bank studies demonstrate the disparity in the amount of supplementary documentation required by different customs offices. While some information is essential, an excess of it ultimately hinders the control function and increases operating costs.

Similarly, unnecessary inspections should be reviewed. It is certainly difficult to define when an inspection is unnecessary, but it is clear that in the current context of international trade, total control is utopian, and certainly, whoever tries to control everything, in reality controls nothing. A technically designed selectivity should involve physical controls on a small percentage of shipments, less than ten percent (10%), supported by intelligent risk management systems and the proactive analysis of information. Generally speaking, facilitation does not imply an absence of control, but rather aims to organize efficient controls appropriate to the nature and particularities of each operation, so that shipments spend minimal time in customs. And when we say minimal, we mean that delays should be those necessary according to the circumstances and particularities of the operation.

The Agreement also promotes regulatory and interpretative stability, essential elements of legal certainty and predictability in business. The Facilitation Agreement makes special reference to these topics, as it is clear that changes in the interpretation of regulations, as well as their retroactive application and the failure to apply the principle of legitimate expectations, violate the principles of transparency and equal treatment enshrined in the General Agreement on Tariffs and Trade (GATT).

Likewise, another issue proposed by the Agreement concerns the coordination between the various State offices working in the border area, as well as the coordination between the customs offices of the bordering countries, a topic that deserves special attention, since the efficiency of one office can be neutralized by the inefficiency of others.

The importance of the Facilitation Agreement lies precisely in placing these issues on the agenda. It serves as a wake-up call regarding cross-border inefficiencies. It highlights that these inefficiencies, resulting in delays and overloads, have a direct impact on costs (transport, containers, insurance, terminals, ports, etc.), while also potentially affecting the quality of goods (e.g., food products) and, at times, jeopardizing business opportunities (e.g., delays in the delivery of seasonal products or delays occurring on specific dates such as Children's Day, Mother's Day, Christmas, etc.).

Moreover, These types of issues have a more diffuse, but no less important, impact on the overall business environment of a given country. Indeed, it is clear that the prevalence of inefficient operating practices that increase costs impacts the business environment by reducing the likelihood of attracting foreign direct investment, preventing countries from participating in global value chains, and raising input prices and reducing business competitiveness.

Thus, facilitation is presented as a set of actions aimed at reducing the time and costs of international trade; it is a way to ensure uniformity on a global scale and faithful compliance with the principles of the WTO.

In short, the principles of effectiveness, efficiency, and expediency must guide all administrative action. Regardless of the sphere of state intervention, citizens require an administration that adequately fulfills its assigned public purposes, acts predictably, and responds promptly where its intervention is necessary.

3. Advance Resolutions (AR)

Certainly, before finalizing a commercial transaction, it is essential for the contracting parties to fully understand the legal consequences of their actions. In the realm of international trade in goods, it is crucial for the importer to have, prior to entering into the transaction, a clear understanding of the goods' tariff classification, applicable duties, any specific regulations that may apply, the restrictions arising from their origin, any applicable tariff preferences, or their potential subjection to antidumping or countervailing duties. An effective legal measure to prevent these uncertainties from turning a potentially good deal into a bad one is to request a binding prior consultation from the customs authorities, who will resolve the matter in question through an advance ruling.

Advance rulings are written decisions issued by the customs administration, at the request of an interested party and prior to the importation of the merchandise involved, through which the treatment to be given to said merchandise at the time of its destination is determined, in relation to the consulted aspects that are relevant for the determination of the applicable tariff, tax and restriction regime.

These are mandatory or binding provisions that the state must observe. This measure has enormous facilitating effects and also provides legal certainty to importers in their relations with Customs, since the resolutions issued by Customs will have the legal nature of a binding nature for it, and therefore the interested party can have a certain assurance that they will not subsequently suffer claims from Customs for the operations that complied with said advance rulings.(4)

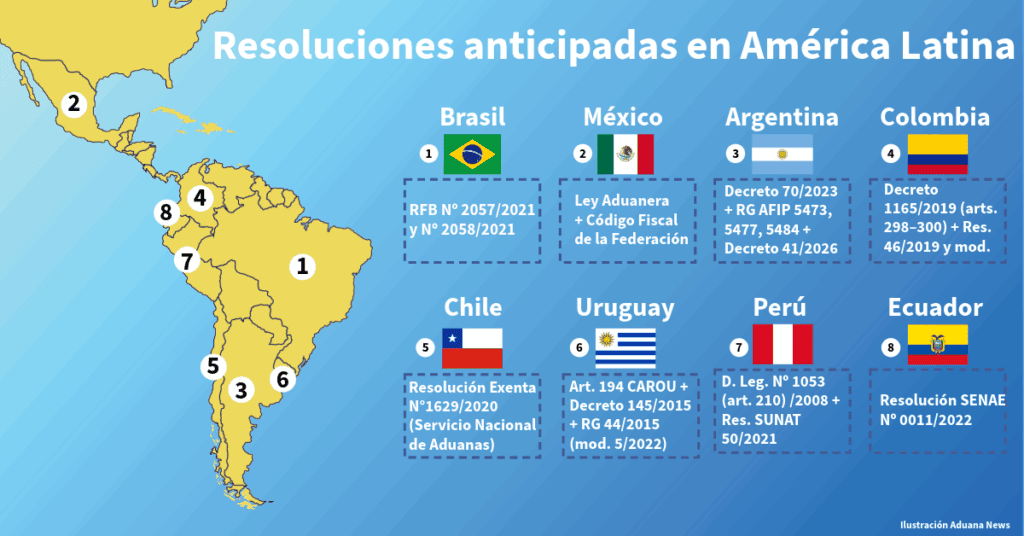

4. The Latin American experience

In Uruguay, the advance ruling procedure is expressly addressed by law, as it is regulated in Article 194 of the CAROU (Customs Code of the Eastern Republic of Uruguay). This article establishes that the holder of a direct and personal right or interest may consult with Customs regarding the application of customs legislation to a specific and current situation.

To this end, the person concerned must present the constituent elements of the situation that motivates the consultation, and is also authorized to express his or her reasoned opinion.

Decree 145/2015 established the regulations for this institution. It states that the resolution will apply to transactions documented subsequently (it is not retroactive). It stipulates that the resolution must be issued within 30 business days of the request. The resolutions must be published, and the applicant's right to appeal is guaranteed.

Subsequently, through General Resolution 44/2015, the National Customs Directorate of Uruguay regulated the consultation procedure. This established the submission requirements, processing formalities, corresponding deadlines, and their consequences. Finally, the Attachments The aforementioned resolution was modified by General Resolution 5/2022, introducing adjustments to the procedure, without altering the legal basis or the substantive effects of the institute provided for in the CAROU and its regulatory decree.

In Brazil, for its part, there is a prior classification consultation regime, established by Resolution of the Federal Revenue of Brazil (RFB) No. 2057 of 2021 and a prior consultation regarding the interpretation of tax and customs legislation regulated by Resolution of the Federal Revenue of Brazil (RFB) No. 2058 of 2021.

The regulations clearly establish who is entitled to submit the request, the requirements that the request must contain, the formalities corresponding to its presentation, the effects that the advance resolution will have, the cases of divergences and its publication.

In Colombia, the Advance Ruling is regulated in Article 298 of Decree 1165 of 2019. It is defined there as the act by which the National Directorate of Taxes and Customs (DIAN), before the importation of goods, issues a ruling regarding the tariff classification; the valuation criteria; the origin; the refund, suspension or other exemptions; the re-importation free of payment of customs duties; the application of quotas and in general any other matter agreed by Colombia through international agreements.

The procedural system was developed by the 46 2019 resolution of and its amendments —39 2021 resolution of y 168 2021 resolution of—, which establish the requirements for presentation, formalities, processing and effects of advance resolutions.

Regarding the deadlines, the article 300 of Decree 1165 de 2019, modified by Decree 659 of 2024It stipulates that the advance ruling must be issued within two (2) months counted from the date of filing the complete application or according to the terms provided in the applicable trade agreement.

The regime was also subject to adjustments by the Decree 360 of 2021, which reinforced the mandatory nature of its application and required the applicant to report any changes in the facts or legal circumstances within the following fifteen (15) days.

Additionally, the 185 2024 resolution of It updated certain operational aspects of the procedure, including the electronic submission of applications to the DIAN and the determination of the competent departments for their handling.

In Chile, the advance ruling system is supported by Exempt Resolution No. 1.629 issued by the National Customs Service, which approves the procedure applicable to the issuance of these rulings and remains in force as the specific regulatory framework on the matter. It defines an advance ruling as the official and binding written pronouncement issued by the National Customs Service, prior to the processing of an import, export, or re-entry declaration, that affects one of the following matters: a) tariff classification, b) customs valuation, or c) rules of origin.

The general requirements for submission are regulated; the necessary documentation; special requirements depending on the classification, assessment or origin; cases of admissibility; procedural issues; issues related to the issuance of the resolution, its validity, publication and administrative review, among other relevant issues.

In Peru, the system of advance rulings is regulated by Legislative Decree No. 1053 (General Customs Law), Article 210 of which establishes that, at the request of a party, the Customs Administration must issue an advance ruling on matters such as tariff classification, the application of customs valuation criteria, the determination of origin, the application of refunds, suspensions or exemptions of customs duties, the re-importation of repaired or altered goods, and other matters provided for in international agreements signed by Peru. The aforementioned law establishes that the rulings must be issued within 90 days of their submission. It also stipulates that they will be effective from their issuance or the date established therein and may be used for other future operations carried out by the same importer, provided that the factual and legal circumstances that motivated their issuance remain unchanged. It also establishes the obligation to publicize it through the institutional portal of the Customs Authority: National Superintendency of Customs and Tax Administration (SUNAT).

Then, through resolution 50/2021 of the SUNAT, specific issues related to prior consultation linked to classification issues are regulated. There is also a Supreme Decree 14/2021 for issues related to advance resolutions of non-preferential origin.

In Mexico, explains Espinosa Berecochea (5), customs regulations address the issue in a general and incomplete manner, and also do not contemplate the possibility of conducting a prior consultation on the origin of goods, regulating consultations on classification and customs valuation matters.

Indeed, Mexican law does not provide for an autonomous and systematic system of advance rulings on customs matters comparable to those existing in other countries in the region. Regulations are scattered primarily throughout the Customs Law and the Federal Tax Code, with customs consultations being integrated within the general framework of tax consultations before the tax authority.

The Customs Law expressly provides for the possibility of submitting inquiries regarding tariff classification, allowing importers, exporters, or customs brokers to request a preliminary ruling on the applicable tariff classification for specific goods. It also addresses provisions related to the determination of customs value, which may lead to prior rulings when there are doubts about the correct application of valuation rules. This procedure is complemented by the general rules established in the Federal Tax Code for processing inquiries regarding real and specific situations.

In Ecuador, for its part, through Resolution 0011 of 2022, issued on February 04, 2022, the National Customs Service of Ecuador (SENAE) issued the procedure that regulates the issuance of advance resolutions.

This resolution establishes the purpose and scope of the institute, stipulating that matters relating to tariff classification, origin, and customs valuation of goods may be subject to advance consultation. It also designates SENAE as the competent authority and establishes the binding nature of the advance ruling with respect to both the Administration and the applicant, under the terms set forth therein.

The regulation also governs the legal effects of the decision, its institutional publication, the formalities of the application, and the general and specific requirements depending on the subject matter consulted. It also addresses aspects related to admissibility and grounds for inadmissibility, withdrawal of the petition, the procedure for issuing and notifying the advance decision, as well as its subsequent publication, among other procedural provisions.

5. The Argentine case. Decree 70/2023, AFIP General Resolutions 5484, 5473 and 5477 and the recent Decree 41/2026

In Argentina, the original Customs Code did not expressly contemplate the concept of advance rulings, a circumstance understandable given the historical context of its enactment, prior to the consolidation of this legal institution in international trade law. Subsequent reforms also failed to incorporate comprehensive regulations on the matter, although in administrative practice mechanisms existed that allowed for obtaining advance rulings in certain areas, particularly tariff classification.

Notwithstanding the foregoing, Law 27.373 approved the Trade Facilitation Agreement, which includes among its commitments the implementation of advance rulings in customs matters. However, the internal regulatory reception of this mechanism only occurred with the enactment of Decree 70/2023. Through Articles 120 and 132 of said decree, Articles 226 and 323 of the Customs Code were amended, incorporating advance rulings for both imports and exports.

It was determined there that the advance resolution is the administrative act, issued by the customs service, at the request of the applicant and prior to the import or export of the merchandise, by which the customs treatment to be granted to the merchandise at the time of its entry or exit is established, in relation to the subject of the consultation.

The request is appropriate in cases of tariff classification, origin, valuation, or in relation to the elements necessary for the correct application of the tax regime, prohibitions or restrictions, thus establishing a broad material scope.

Furthermore, it was stipulated that the regulations would determine the formal requirements and the information that the applicant must submit. The system established a period of thirty (30) days for the issuance of the advance ruling. In the event of silence from the administration, the declarant was authorized to formalize the customs declaration in accordance with the procedure established in the Customs Code for declarations involving the customs service (Article 234, paragraph 3, for imports and Article 332, paragraph 3, for exports), and the provision of sufficient guarantee may be required. The possibility of filing an appeal against the advance ruling issued was also provided for, as outlined in Article 1053, subsection f), of the Customs Code.

To implement the system established by Decree 70/2023, the following resolutions were issued: General Resolution AFIP 5473/2023, which regulates advance rulings on tariff classification; General Resolution AFIP 5477/2023, concerning valuation; and General Resolution AFIP 5484/2024, regarding customs technical criteria. These regulations fully comply with the Technical Guidelines on Advance Rulings on Customs Classification, Origin, and Valuation, issued by the World Customs Organization (WCO) in 2018.

Subsequently, Decree 41/2026, published in the Official Gazette of the Argentine Republic on January 26, 2026, introduced adjustments and clarifications to the system established by Decree 70/2023, systematizing its regulation and more precisely defining its scope, procedures, and legal effects. Although the formal incorporation of the system into the Customs Code had occurred in 2023, it was this decree that consolidated its organic treatment within the customs system.

The decree defines its scope, procedural requirements, and legal effects; establishes the matters subject to consultation; sets forth the formal and substantive admissibility requirements; regulates the issuance deadline and its validity period; and establishes its binding nature for the customs service with respect to the applicant, provided that the customs declarations strictly conform to the facts, background, and legal grounds declared. It also addresses the circumstances under which the decree may be modified, revoked, or lost, such as regulatory changes, substantial variations in relevant circumstances, or inaccuracies in the information provided, and establishes mechanisms for publicizing the adopted criteria, with due regard for the protection of confidential information.

Notwithstanding this consolidation of domestic regulations, it should be noted that, in the multilateral arena, the Republic of Argentina notified the World Trade Organization of an extension to the final date for the application of Article 3.9(a)(ii) of the Trade Facilitation Agreement, concerning advance rulings on rules of origin. Through communication G/TFA/N/ARG/1/Add.4, distributed on January 9, 2026, it was reported that the originally agreed-upon date (namely, January 23, 2026) was extended to July 23, 2028. The request was submitted in accordance with the extension mechanism provided for in Article 17 of the aforementioned Agreement and was based on the need to allocate resources sequentially to address existing trade facilitation challenges within the framework of the foreign trade normalization process.

It should be noted that this notification was distributed prior to the publication of Decree 41/2026, which occurred on January 26, 2026. This demonstrates that the extension of the international deadline was due to a rescheduling of the compliance timeline assumed within the framework of the Agreement, without disregarding the subsequent internal regulatory consolidation of the institute.

In this context, the deferral is relevant for the systematic analysis of the Argentine regime, as it demonstrates that, even though the advance ruling is formally incorporated into the Customs Code and regulated in various matters, the specific commitment assumed at the multilateral level regarding advance rulings on origin was subject to an extension in its final implementation date.

Thus, the institute is integrated into the Customs Code system and regulated internally, articulated with the provisions relating to classification, origin and valuation; however, at the international level, the Argentine Republic notified the extension of the implementation period provided for in article 3 of the Agreement, in accordance with the mechanism contemplated in its article 17.

6. In closing

The current dynamics of international trade impose logistical schemes that are increasingly oriented towards schemes “just in time, which require increasingly shorter border crossing times. This does not, of course, diminish the essential control function of Customs, whose primary purpose remains the oversight of the entry and exit of goods, the protection of tax revenue, and the safeguarding of the State's economic and non-economic interests.

The most efficient countries are the most competitive and facilitation tends to ensure agile and efficient customs processes, in order to promote the reduction of direct and indirect costs linked to international trade, in order to increase the competitiveness of companies and thus improve their performance, which in turn will generate greater economic growth.

In this context, the incorporation and consolidation of the advance rulings regime in Argentine customs legislation, starting with Decree 70/2023 and its subsequent systematization by Decree 41/2026, constitutes a significant advance.

The institute allows for the definition, prior to the arrival or departure of goods, of issues relating to the tax regime, classification, origin or applicable restrictions, reducing uncertainty and avoiding subsequent disputes.

Notes and references

1.COTTER, Juan Patricio, “The facilitation of legitimate trade. Reality or Utopia”, Tarifar Magazine No. 470, January 2023.

2.COTTER, Juan P. “The challenge of Customs in the 21st century. Facilitation and control”, in AA VV Information technology in Customs and its legal effects, Mexico, Argentina and Colombia. (coord. Nohemí Bello Gallardo), University Foundation of Law, Administration and Politics SC, Mexico, 2012.

3. GUICOVSKY LIZARRAGA, Ezequiel, senior officer of the International Trade Centre, which is the joint agency of the WTO and the UN // Seminar organized by CERA and ITC in Buenos Aires in March 2017

4.ROHDE PONCE, Andres, “Trade Facilitation”, ed. CAAAREM, Mexico, 2021, p. 213.

5. ESPINOSA BERECOCHEA, Carlos, “Legal Regime of Advance Resolutions in Foreign Trade Matters”, Praxis Journal of Fiscal and Administrative Justice.

Attorney (UCA), Partner at Petersen & Cotter Moine Law Firm.

Full Member of the Argentine Institute of Customs Studies (President 2010/2011). Active Member of the International Academy of Customs Law (Member of the Board of Directors 2015/2023). Active Member of the Argentine Association of Tax Studies. Member of the Customs Law Commission of the Council of the Center for Studies of Financial Law and Tax Law, of the Department of Business Economic Law of the Faculty of Law of the University of Buenos Aires. Member of the Scientific Committee of the Journal of the Colombian Institute of Tax Law.

Professor of customs law in the postgraduate courses in customs law at the University of Buenos Aires, where he is also the Vice President of the Customs Law Update; of the Catholic University of Argentina, of the Austral University and of the Di Tella University.

Author of the books “Customs Law and International Trade”, published in 2018 by Guía Práctica; “Customs Law”, published in 2014 in 3 volumes by Abeledo Perrot, winner of the 2014 Argentine Association of Tax Studies Award for the book of the year; “Customs Offenses”, published in 2011 and second edition in 2013 by Abeledo Perrot; and Coordinator and co-author of the books “Customs Law Studies”, published in 2007 by Lexis Nexis and “Customs Law Studies. 30 Years of the Customs Code”, published in 2012 by Abeledo Perrot. He was one of the updaters of the Annotated Customs Code, published in 3 volumes by Abeledo Perrot in 2012.

He has also participated in collective books published abroad and has published more than fifty articles related to customs law, published in various media (La Ley, El Derecho, Jurisprudencia, Revista de Derecho Fiscal, Revista de Estudios Aduaneros, Revista Tribunas, and La Nación newspaper).