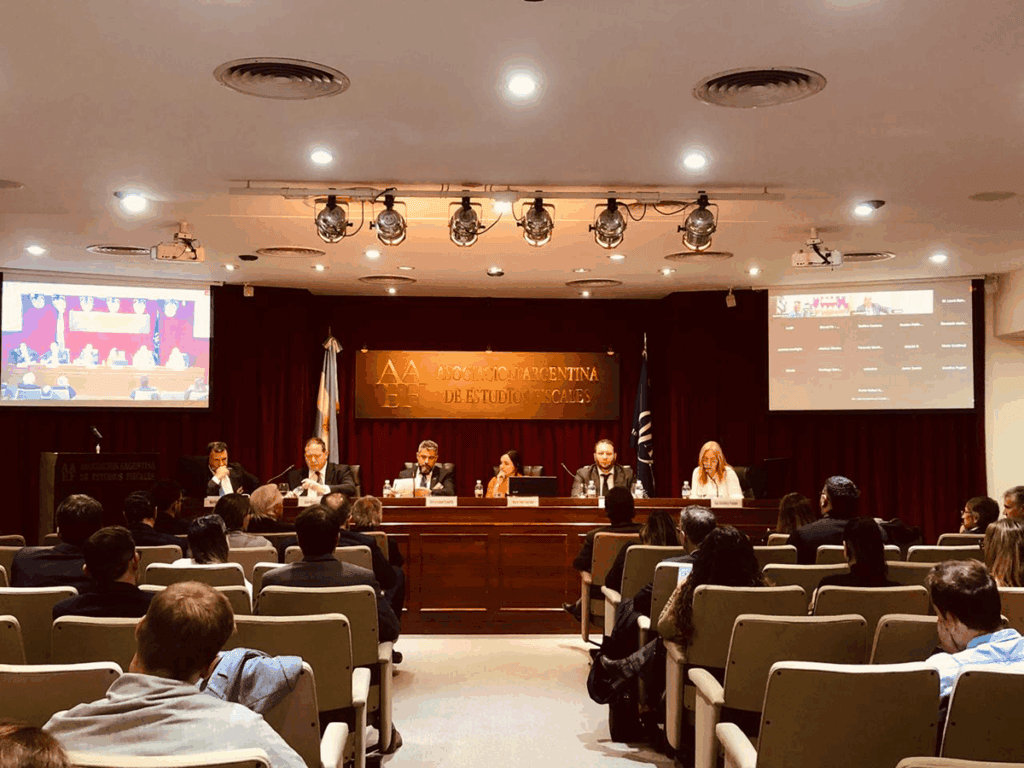

With an agenda of 24 distinguished speakers, more than 200 accredited attendees, and an attendance of more than one hundred in-person participants, among whom the active participation of young people stood out, the Argentine Association of Fiscal Studies (AAEF), at its headquarters on Julio A. Roca Avenue in the City of Buenos Aires, once again welcomed the academic, professional, and institutional community to the XNUMXth International Conference on Customs Law.

This biennial meeting, established as a space of excellence for analysis and debate, reaffirmed its commitment to the development and advancement of the discipline, addressing its current situation and the latest theoretical and doctrinal advances. The 2025 edition took place on August 7 and 8, organized around two thematic areas and a roundtable discussion that attracted the interest and active participation of all those present.

Institutional Opening

At the opening, the Dr. Alejandro Messino, President of the AAEF, He expressed his gratitude to those who made the development of the Conference possible, highlighting the Scientific Committee chaired by the Dr. Catalina García Vizcaíno and Dr. Gustavo Zunino, to the members of the event's Executive Committee and to all the people who contributed to us being here today, marking the beginning of such an important meeting.

During his speech, Dr. Messino referred to the current situation in Argentina and the world, noting that "in times of great economic and social challenges, both locally and globally, the dialogue promoted by this Conference becomes more necessary than ever to find contributions tailored to reality."

Then the speaker took the floor Dr. Miguel Licht, President of the National Tax Court (TFN), who began his inaugural address with a profound reference to the Talmud to illustrate the legal philosophy that guides his thinking: “Lo ba-shamayim hi—the law is not in heaven.” He explained that this maxim means that the interpretation of the law belongs to the human realm and must be based on a rational, communal construction, grounded in principles, context, and a sense of justice.

Relating this principle to international trade, Dr. Licht argued that “customs valuation must respect the economic architecture and not just the formal trappings of private contracts.” In particular, he noted that the application of the Article 8.1.c of the GATT Valuation Agreement It cannot be limited to the literal meaning of the contract, but must consider the economic reality of the operations and the effective link between royalties and imported products.

"The contract is a sign, not an oracle," he affirmed, emphasizing the need for a "down-to-earth" interpretation that prioritizes economic substance over mere formality. He emphasized that interpretation requires tradition, principles, reason, and the courage not to submit to what the powerful party attempts to impose as contractual truth.

Finally, the Dr. Marcelo Mignone, Deputy Director of the Customs Legal Technique Subdirectorate (TLA) of the Customs Regulation and Control Agency (ARCA), highlighted the importance of the event for the scientific advancement of tax and customs law, congratulating the AAEF for “organizing this event methodically since 2008.”

He emphasized the DGA's commitment to maintaining a permanent and close relationship with the private sector, noting that "we generate and maintain close ties with the various players in foreign trade, seeking to resolve the various challenges that arise in daily life."

To this end, Dr. Mignone made special reference to the impact of the Decree of Necessity and Urgency (DNU) 70/2023 and explained that, for its implementation, "we created an inter-area commission to identify, analyze, study, and implement these measures," with subgroups specializing in regulatory, operational, and IT matters.

Among the advances he mentioned the modification of the General Resolution 2570 which "removed importers/exporters and customs brokers from special customs registries," implementing a system that enables profiles to document operations by validating only "the criminal record certificate."

He also highlighted the General Resolution 5474, which "establishes the procedure for the advance declaration of goods, facilitating direct dispatch to the market," and the implementation of advance resolutions that "provide security for the declarations submitted by foreign trade operators."

Regarding guarantees, he explained that "a paradigm shift has been introduced in terms of requiring them for destinations suspected of infringement," allowing them to be requested "after the goods have been released," which simplifies procedures and reduces costs.

He mentioned that, thanks to these measures, "of 51.000 actions that are processed in December 2023, today they are at 39.000", achieving a 25% reduction in approximately 18 months.

Finally, he emphasized the Argentine Customs' commitment to "regulatory simplification, operational simplification, digitization of procedures, and reduction of operating costs," without sacrificing "its primary function of proper customs control." He asserted that "any measures that may be adopted in the future will arise from ongoing collaboration between the various departments of the state and the active participation of the private sector."

Customs valuation

Panel 1, chaired by Christian Gonzalez Palazzo, with Rufino Beccar Varela as a reporter and Juan M. Sanz As secretary, he addressed General principles of taxation and customs duties, with special emphasis on determining the tax base under the GATT Valuation Agreement and the Customs Code. Complex cases, successive sales, exports of primary products, regulation of royalties, and current disputes were analyzed, with particular attention paid to doctrinal and jurisprudential interpretation.

To this end, the guidelines observed at the panel took as their starting point Decree No. 70/2023, through which the Executive Branch issued a relevant instruction regarding the country's situation. In particular, Article 3 was highlighted, which establishes the need to promote greater integration of the nation into international trade, fostering a deregulation policy and adapting the regulatory framework to international standards for trade in goods and services. This includes harmonizing the internal regime of the MERCOSUR member states and complying with the recommendations of the World Trade Organization (WTO).

It was emphasized that the objectives of regulating and facilitating operations, as well as streamlining procedures, require a review of customs processes, especially with regard to customs valuation. This evaluation must be aligned with the guidelines of the World Customs Organization (WCO), the GATT Valuation Agreement, and complementary domestic regulations.

In this framework, they presented from the Eastern Republic of Uruguay, doctors Pablo Labandera and Daniel Olaizola, who addressed the current status of customs valuation in their country. They focused on the declarant's obligations and opportunities in determining the customs value of goods and on disputes related to adjustments for advertising expenses and storage delays. They explained that Uruguay incorporated the GATT Valuation Agreement into its legal system, complementing it with internal regulations that define specific concepts—such as transportation and logistics—that must be included in the tax base for customs value.

They highlighted the particular responsibility of the customs broker as declarant, who must accurately record data related to tariff classification, valuation, and tax allocation, supported by commercial documentation. In this context, the Single Customs Document (SCD) includes a value annex that inquires about the relationship between buyer and seller, royalties, commissions, and other adjustments contemplated in the Valuation Agreement. The importer may voluntarily submit a "subsequent declaration of value and relationship" to provide advance information on the circumstances of the transaction; although its failure to do so does not entail penalties, it may raise presumptions in audit proceedings.

The presenters emphasized that the Uruguayan system prioritizes transaction value in accordance with the GATT Valuation Agreement, allowing secondary methods only in specific cases. They also referred to optional and necessary expenses—such as transportation, cargo, and insurance—that are part of the calculation basis, noting that an internal provision (Agenda 01/03) introduces a controversial interpretation regarding the inclusion of certain costs in free trade zone transactions.

The core of the debate revolved around advertising expenses. According to the speakers, Uruguayan customs considers that when these expenses are assumed by the importer under a contract, they constitute a condition of sale that justifies an adjustment to the customs value, interpreting this as equivalent to an indirect payment to the seller. This position is based on a Brussels definition that, in the opinion of the speakers, contradicts the GATT Valuation Agreement, which only allows these expenses to be included in specific cases, such as when a payment to the seller is agreed upon for advertising not executed.

Drs. Labandera and Olaizola described this interpretation as illegitimate, as it violates the principle of transaction value and ignores the evolving international legal framework, even within the framework of domestic provisions.

Then they participated by Argentina, doctors Bastiana Locurscio and María José Etulain, the latter from Miami.

La Dr. Bastiana Locurscio He presented an in-depth analysis of the conceptual and practical challenges related to the tax base for customs duties. He emphasized that the tax base constitutes the material element of the taxable event and is essential for quantifying the tax obligation along with the applicable rate. While the tax base is traditionally associated with the taxable capacity—linked to income, assets, or consumption—in the case of customs duties, which are considered extra-fiscal, this concept becomes more complex due to additional objectives such as environmental protection, public health, and the defense of national industry, which do not always prioritize tax collection.

He analyzed various doctrinal positions that interpret consumption as an indirect manifestation of wealth or individual exploitation of social resources, highlighting the Supreme Court's criterion, which requires that the tax base be reasonable and consistent with the taxable event, allowing for a certain legislative flexibility except in cases of arbitrariness. He also proposed a classification between bases and parameters, and between general and specific bases, placing special emphasis on antidumping duties, which partially escape GATT regulations.

He then addressed customs duties, particularly the statistical tax, raising questions about their relationship to the cost of the service and their protective function. He concluded by highlighting the importance of an integrative theory of the tax base that considers constitutional and tax principles, especially in customs matters, where extra-fiscal purposes and legislative techniques generate tensions.

Then the Dr. María José Etulain He offered a clear and graphic analysis of the tensions between the World Trade Organization (WTO), the Organization for Economic Cooperation and Development (OECD) guidelines, and Argentine domestic law regarding customs valuation. He focused on a recent ruling regarding a value adjustment applied in 2009 to an Argentine company that imported glyphosate at questionable prices compared to its competitors. He highlighted the application of the Article 2 method of the WTO Valuation Agreement and noted that the ruling reaffirms the principle of legality, limiting the application of OECD guidelines to customs valuation and confirming the primacy of WTO rules incorporated into Argentine law.

En particular, el president of Panel 1, Christian González PalazzoHe concluded by noting that, above all, we must celebrate each academic meeting by recognizing the importance of Catalina García Vizcaíno, the guiding force behind these events. She has been the driving force behind these meetings, which bring together experts from diverse backgrounds but with a common goal: to enrich customs law through debate and reflection.

Customs law, as a science, faces—according to jurisdictional practitioners—new and ongoing challenges. These challenges require starting from a fundamental principle: although customs law draws on other sciences, it possesses sufficient autonomy and identity to respond to the complex problems arising from its specific dynamics.

Customs Procedures

El Panel ii, chaired by Harry Schurig, had Martín Yannielli as a reporter and Ana Pampín as secretary. This space considered the rules governing administrative and customs procedures, analyzing the aspects that regulate operations and management.

The panel's central focus revolved around the effective protection of constitutional rights and guarantees in customs operations, as well as the efficiency and speed of procedures, legal certainty, reasonable deadlines, and newly introduced remedies.

In this context, they explained Dr. Juan Manuel Soria (Member of the National Tax Court); Dr. Pablo S. Borgna (General Directorate of Customs); and Dr. María Noel Lascano (private sector); along with Eugenia Rodríguez Campos (Director of VUCE); and Gastón Miani (expert in Criminal, Tax, and Customs Law).

El Dr. Juan Manuel Soria He addressed the issue of excessive delays in customs infringement proceedings and the right to obtain a resolution within a reasonable period. He critically analyzed the development of jurisprudence and doctrine regarding statutes of limitations, warning of the risks of judicial arbitrariness when legal provisions are interpreted using subjective criteria to determine the reasonableness of deadlines.

He defended the strict application of the statute of limitations of the Customs Code, updated by Decree 70/2023 and Law 27.742, and maintained that reliable notification of administrative acts of individual scope that affect subjective rights or legitimate interests is an essential condition for guaranteeing procedural legislation and legal certainty.

Furthermore, he proposed that the solution to problems related to reasonable deadlines should not be left to judicial discretion, but rather to the legislator who should establish clear rules. He rejected flexible interpretations that allow judges to deviate from the letter of the law to decide based on subjective criteria, as this would undermine legal certainty and the predictability of the system.

He emphasized that the reform introduced by Decree 70/2023, which requires notification of both the opening of the investigation and the conviction, tends to neutralize problems related to reasonable deadlines and strengthens the customs regime. However, he warned that the persistence of administrative or commercial interpretations contrary to the law can perpetuate legal uncertainty and affect the protection of rights.

Dr. Soria also pointed out that even without the amendment introduced by the decree, there is no legal loophole in the Customs Code regarding Customs' obligation to notify the opening of the investigation and the conviction. In this regard, he distanced himself from positions proposing greater judicial flexibility and emphasized that any changes to the time limits or effects of the statute of limitations should be the exclusive responsibility of the legislator.

Finally, the Tax Court member emphasized the importance of reliable notification as an essential guarantee of the right to defense and the validity of administrative acts, agreeing with other panelists on the centrality of effective communication in customs procedures. To this end, he emphasized the need to strictly and consistently apply the provisions of the Customs Code, a distinguished legislative work resulting from the work of specialized legal experts.

The following exhibition was by Dr. Pablo S. Borgna, who developed the theme "The review of customs resolutions and the guarantee of sufficient judicial review: an analysis of the appeal system following the reform of Decree 70/2023., limiting his analysis to the appeals available to the public against customs administrative resolutions that do not allow for repetitions, reject appeals, or impose sanctions (customs violations). He emphasized that the possibility of reviewing administrative resolutions issued by Customs reinforces the doctrine of the guarantee of sufficient judicial review and consolidates the principles of the republican system of government. He also evaluated the impact of Decree 70/2023 and any other regulations that affect the legal review mechanisms applicable to such resolutions. In this regard, he considered that the Law of Bases and Starting Points for the Liberty of Argentines (Law 27.742) and Decree 695/2024, while not including amendments to the Customs Code, recognizes that some reforms to administrative law by both regulations had an impact on customs law, specifically, in the area of appeals addressed in his presentation.

Based on the jurisdictional powers of administrative bodies, recognized by the Supreme Court of Justice (SCJN), and this premise being legally accepted in our system, he indicated that it is the General Directorate of Customs, as the state body specialized in customs matters, that must rule the law in accordance with the regulations governing said authority. The National Tax Court, another body dependent on the Executive Branch, albeit with greater autonomy, may review the decision of the former, acting as the reviewing body of that administrative act, replacing the decision issued by the Court of First Instance. He then proceeded to a detailed analysis of the different avenues for appeal. He emphasized that the regulations applicable to appeals allow the citizen to voluntarily choose to submit to the procedure before the National Tax Court, and may also opt for a judicial process, that is, to appeal to the competent judge. However, he clarified that the regulation imposes limitations on this optional appeal mechanism, depending on the nature of the administrative procedure and the related amounts.

Regarding those cases of optional appeals before the National Tax Court or administrative litigation claims, he considered it relevant to highlight the differences between the two, reflecting on everything that the advantage of "choosing" the type of process assisted by a lawyer entails. To this end, he described seven disparities between the two processes: 1) "Ex officio vs. party impetus": This is equivalent to deciding not to apply the expiration of the instance to the first instance of review (before the TFN) or choosing to voluntarily submit to said institute (by going to the first instance of Justice); 2) The search for the material truth of administrative law: Although it arises from the principle of legality and, in accordance with this, is applicable to both review systems, before the Tax Court, a system of review of the administrative act is chosen in which this principle is applied in a more refined manner or with greater intensity; 3) The constitutional validity of tax or customs laws and their regulations: Considering that the Tax Court is prohibited from ruling on their unconstitutionality, except when the jurisprudence of the Supreme Court of Justice of the Nation has already declared it, while in a judicial process, the Judge may declare, "even ex officio," the unconstitutionality of laws in general; 4) System of opposition of exceptions: Observing that the one enshrined in art. 1149 of the Civil Code of the Nation differs slightly from the system of opposition of exceptions in art. 347 of the Civil and Commercial Procedure Code of the Nation and differs notably from the system of opposition of exceptions in art. 37 of the Federal Criminal Procedure Code (both by application to the case of art. 1179 of the Civil Code); 5) Deadlines and forms: They present different rules of the game regarding the forms and applicable deadlines; 6) Computerized system: Before the Tax Court, this involves the use of the "TAD" system (governed mainly by Annex II of Resolution 43/2019 of the Secretariat for Modernization) instead of the "Lex 100" system (governed mainly by regulations issued by the Courts themselves, especially the Supreme Court of Justice); 7) Fee: Before the Tax Court, a Court Fee is paid (2,50% of the disputed amount), to which (in the event of an appeal against the TFN ruling before the CAF) the "Court Fee" (3% of the disputed amount) will be added. Dr. Borgna observes that, although both concepts are part of "the costs of the trial" and the expectation is that the defeated party will pay them, it is no less true that by going to court, the taxpayer would ensure "saving that 2.50%." This percentage may be considered irrelevant, but in cases of great economic impact, it constitutes a risk worth considering.

When addressing the differences between the appeal of a decision rendered before the National Tax Court and those before the judge as a result of the contentious claim in the first instance, he made several notable considerations, among which he indicated that if the taxpayer, when choosing the "review route" of the customs resolution, voluntarily and with mandatory legal representation, opted to appeal to the Federal Tax Court (TFN) when he could have gone to court in some way, then that content, which is strictly outside the jurisdiction of the TFN's ruling, should not be reviewable. He supported this by asking: What did the Tax Court rule that should have been ruled differently? Therefore, when the TFN is asked to declare an unconstitutionality (not previously declared by the Supreme Court of Justice), the answer will be: nothing at all. Therefore, there would be no grievances to express, since art. Article 265 of the Constitutional Court requires the appellant to present "a specific and reasoned criticism of the parts of the judgment that the appellant considers erroneous." In this case, the term "judgment" refers to the ruling of the Federal Tribunal for National Defense (TFN), which supersedes the first-instance ruling. Therefore, those issues that were erroneously submitted to the TFN for consideration should not be reviewed. Furthermore, given the impossibility of declaring the lack of constitutional validity of tax or customs laws and their regulations, the party could choose to bring its claim to the TFN, seeking an additional award of costs against the State, by adding to the first-instance work the fees related to the tasks that must be performed later in the Court. Dr. Borgna should note that the customs appeal system is not exempt from the provisions related to the abuse of rights (Article 10 of the Civil and Commercial Code), since Chapter 3 of the Preliminary Title of the aforementioned Code regulates, in general terms, the exercise of rights. He also noted that Article 25 of Law No. 27.742 (Official Gazette 8/7/2024) incorporated Article 1 bis, paragraph c) into Law 19.549 (LNPA), clearly stating that "Both the Administration and the citizens must act in good faith and loyalty in the processing of procedures." He believes that the customs appeal system should be integrated with the way in which rights must be exercised, given the limitations inherent to the TFN, and thus a coherent and harmonious legal system will be obtained, understood as a whole, imbued with logic and good faith.

We conclude that, in cases where the two-way option—optional and exclusive—is available, the citizen should analyze the optimal review process, taking into account their claim. To this end, the differences between each process should be considered, as indicated above, noting that the review process (TFN or contentious claim before a judge) has advantages and disadvantages, which the citizen is aware of or should be aware of.

Finally, he warned that it is necessary to reform Article 1025 of the Civil Code, since the $25.000 fee required to access the Tax Court has become outdated. Furthermore, to further improve the statistics, as well as the time taken to issue rulings, there are two paths: creating more Chambers or reducing unproductive access to the Tax Court. He invited the customs community to consider these two specific axes that will strengthen the appeal system, proposing an additional Customs Chamber (it could be Chamber H, equating tax appeals with customs appeals) and increasing the amount of challenge required to access the Tax Court (Article 1025 of the Civil Code), which, as he pointed out, has become completely outdated.

Then the Dr. Noel Lascano presented the topic "The omission of the hearing in the procedure for violations: A useless ritualism or a violation of due process?”. His presentation focused on a detailed analysis of a real case, in which the hearing procedure provided for in Article 1101 of the Customs Code has been omitted within the framework of a procedure for violations, which violates the guarantee of the due right of defense enshrined in Article 18 of the National Constitution. Recalling that the principle enshrining the guarantee of due process has been extended to the defense of the rights of individuals before the Administration, and the same occurs with the principle of effective judicial protection, whose projection, in administrative venue, has been highlighted by doctrine. He also emphasized that the National Law of Administrative Procedures, in its current wording, recognizes in its Article 1 bis paragraph a) the right of citizens to effective administrative protection. Therefore, the Administration, to duly ensure this right, must respect, at all times, the right of individuals to be heard, to offer and produce evidence, to obtain a reasoned resolution and to the development of a procedure without delays, which are processed and concluded within a reasonable period.

Thus, Dr. Lascano observed that there are legal consequences for the Administration's failure to comply with the most basic procedural guarantees for violations. She used a case study to demonstrate how the failure to observe key procedural steps—such as the correct formulation of the order opening the investigation and, more importantly, the hearing of the proceedings—results in the absolute nullity of the procedure, with direct effects on the statute of limitations for the Treasury's actions to collect taxes governed by customs legislation.

After presenting the specific case, it carries out a detailed analysis of the flaws that arise in the administrative process, dividing them into three stages: 1) The flaw at its origin: the nullity of the order opening the summary due to non-compliance with the provisions of Article 1094 of the Customs Code. Consequently, the fiscal action is subject to a statute of limitations; 2) The central flaw: the failure to review the administrative proceedings. The nullity of the customs resolution; and 3) The flaw at its end: the late notification of the appealed resolution. The statute of limitations for the fiscal action is subject to a statute of limitations.

Regarding the order opening the preliminary investigation, he emphasized that it is a significant administrative act in the procedure for infractions. First, because it constitutes the first intervention of the administrator who, faced with the possibility of dismissing the complaint or ordering an extension of the investigation, decides to order the opening of the preliminary investigation, believing there are sufficient grounds to initiate the procedure, in order to determine whether the reported facts constitute a customs violation and, if so, to determine those responsible for said violation. And, second, because it constitutes the act prior to the resolution, which provides for the alleged perpetrators to be given a review of the proceedings so that they may present their defenses. Therefore, the precise establishment of the facts constituting the infraction, the verification of the infringing merchandise, its tariff classification and valuation, the receipt of the declarations from the alleged perpetrators, the liquidation of any applicable taxes, and the other steps leading to the clarification of the facts under investigation must not be omitted. In this case, as in the example given, its omission imposes the nullity of this administrative act and consequently the absence of generating the effect of interruption or suspension of the prescription of the action to impose penalties and pursue the collection of taxes.

Regarding the administration's duty to inform the alleged perpetrators of the proceedings so they can defend themselves and offer evidence, he recalled that Article 1101 of the Code provides that, once the measures provided in accordance with Article 1094 have been fulfilled, the administrator will be given access to the proceedings, and as established in Article 1103 of the Code, this has the effect of notification of the liquidation of taxes referred to in Article 1094, paragraph d). This situation has not been met in the case brought as a witness. Consequently, there has been no opportunity for the administrator to present its defenses before the issuance of the customs resolution, nor, of course, to offer and produce the relevant evidence. Highlighting that the only notification sent to the entity was made solely to inform it of the resolution issued at the customs administrative headquarters, which reveals a clear violation of the provisions of Article 1101 of the Customs Code, in addition to the failure to comply with the provisions of Article 1037, paragraph f) of the Customs Code, which establishes that the acts that grant the opportunity to present a defense in the procedure for infractions must be notified to the accused. Thus, Dr. Lascano emphasizes that, in this case, the customs service violates not only the importer's right to defense but also the most basic principles of procedural law and due process, as recently understood by the Tax Court in cases similar to the one analyzed here, distorting the procedure, which is not remedied by the notification of the final Customs resolution.

To then refer to the final defect, regarding the late notification of the customs resolution. Indicating that in the case under analysis, the customs resolution was issued on December 26, 12, and notified to the importing company on February 2024, 3. Noting that the notification of administrative acts is of transcendental importance in the administrative procedure. Reflecting in the case, even though the order opening the summary would have had the effect of interrupting and/or suspending the statute of limitations, the notification of the appealed resolution was carried out when the prescriptive period had already largely expired, without any evidence of the existence of another act prior to the issuance of the appealed resolution that, according to the applicable regulations, has the effect of interrupting or suspending the statute of limitations, nor reasons that justify the delay by the customs service in timely notification of the act in question. This, without prejudice to pointing out that the administrative proceedings were completely paralyzed for almost five years from the issuance of the order opening the summary (02/2025/26) until the request for clarification made to the reporting area, both with respect to the alleged infraction and the amounts demanded (12/2019/12). In this regard, Dr. Lascano recalled the importance of the principles of certainty and legal security that must be safeguarded in the procedures, since, as the Tax Court also holds, "a contrary solution could mean that Customs notified at any time (for example, after several years, five-year periods, decades, etc.) a resolution dated before the statute of limitations began, with the consequent uncertainty regarding the rights of the users." Adding that, in this case, all reasonable parameters for the duration of a customs infringement process were exceeded, in clear violation of the right of the citizens to obtain a ruling without undue delay.

In her final reflections, Dr. Lascano noted that the due process guarantees inherent in judicial proceedings have expanded to include any process or procedure that affects a person's rights. She noted that in a scenario such as the one described, validating a tax charge under the conditions analyzed here—where the procedure is plagued by insurmountable flaws that prevented the taxpayer from being heard—implies degrading constitutional guarantees to the status of mere formalities. Endorsing this approach legitimizes arbitrariness and undermines legal certainty, a fundamental pillar of the relationship between the Treasury and taxpayers. She emphasized that the preambular objective of "enforcing justice" is seriously betrayed when the administrative procedure, rather than being a path to truth and legality, becomes a pointless ritual. An administrative act that arises and develops outside of fundamental guarantees can only generate a null and unenforceable result. Because, of course, justice that is unjust is not justice.

Meanwhile, Eugenia Rodríguez, Director of the Single Window for Foreign Trade Project (VUCE) gave a presentation on this modernization tool, highlighting its key role in the organization and efficiency of trade procedures in Argentina. He emphasized the significant progress made in the digitalization and centralization of information and documentation required for exports, imports, and customs transit.

One of the most relevant aspects of his presentation was the reduction in costs and operational times for users, thanks to the VUCE's ability to streamline procedures and centralize management, providing benefits not only to foreign trade operators but also to the transparency and predictability of the customs process, strengthening the security and confidence of those in charge.

Rodríguez also highlighted the VUCE's interoperability with other systems, as well as its specific tools, including the case law search engine and the tariff item module, among other features.

Another relevant point was the contribution of the VUCE to the speed and efficiency of procedures, streamlining processes and facilitating customs control. Finally, he emphasized that the VUCE meets Argentina's international commitments regarding trade facilitation and customs modernization.

Finally, Panel II featured the presentation of Gastón Miani, who addressed a highly topical issue: the impact of the implementation of the Federal Criminal Procedure Code in the investigation of customs crimes.

The lawyer, who specializes in criminal, tax, and customs law, emphasized that the federal criminal procedural reform represents a paradigm shift. Under the new system, the Public Prosecutor's Office directs the investigation, the investigating judge oversees the legality of the proceedings, and the trial court issues a verdict, ensuring impartiality and respect for the rights and guarantees of the parties.

One of the central points of his presentation was a description of the guiding principles of the new system: oral proceedings, immediacy, adversarial proceedings, publicity, speed, and impartiality. He emphasized that these principles not only seek to streamline processes but also strengthen transparency and the participation of all parties, including the victim—in this case, Customs.

Miani emphasized the importance of training judicial officials in oral investigation techniques and the need for effective coordination between public agencies and specialized technical bodies, such as Customs itself.

He also explained that the new code redefines the organizational and functional structure of the criminal process, establishing clearly differentiated stages with specific objectives, defined timeframes, and institutional actors with specific responsibilities. Among these, he mentioned the preliminary investigation, the investigation oversight hearings, and the oral and public trial.

Regarding customs offenses, he noted that the code offers more effective tools for investigating crimes such as smuggling, customs fraud, and money laundering. He also highlighted the possibility of applying alternative solutions to criminal conflicts, which would allow for a more agile response in certain cases.

However, he cautioned that there is still no uniform approach to the application of these institutions, as some jurisdictions have implemented them more frequently while others have been more restrictive in their use.

In conclusion, the president of Panel II, Harry Schurig, stressed that "many of the problems analyzed during the day, such as administrative bureaucracy and the need to reform procedures, have already been addressed on previous occasions without effective legislative solutions." However, he emphasized that "What Congress didn't solve, technology did; now the law is racing to catch up with it."”, highlighting the transformation that the customs sector is undergoing.

Schurig emphasized that "this transformation will have a significant impact on the processes and actors involved in foreign trade, with more streamlined procedures, more efficient controls, and greater digitalization that will contribute to optimizing operations and reducing administrative burdens." With a reflection that combined humor and seriousness, he urged "continuing to deepen our knowledge of customs law and new technologies, encouraging everyone to train and actively participate in these processes of change."

International Panorama

True to its tradition, these Conferences paid special attention to the international situation. In this context, the Round table titled "Current challenges of international trade: the principles that inspire the GATT and the tariff war, multilateralism and regional agreements. presided over by Gustavo Zunino and composed of Andrés Rohde Ponce (Mexico), Flavia Figueredo (Uruguay) and Héctor Juárez (Argentina).

The debate was opened by Dr. Gustavo Zunino who is He referred to the "multilateral trading system based on principles such as most-favored-nation rights, non-discrimination, tariff reduction, and transparency," along with the "requirement of prior consultations to resolve trade disputes." He noted that "the GATT initially lacked effectiveness due to the absence of a formal dispute settlement system," a situation that changed with the creation of the WTO in 1994 and the Marrakesh Agreement, which "established effective mechanisms for enforcing the rules."

He emphasized that, since then, "global trade has grown steadily," with the United States as the leader until the 2008-2009 crisis and the incorporation of China in 2001, whose "rapid growth transformed global dynamics." Currently, "the United States' protectionist measures, with high tariffs, reflect trade tensions with geopolitical and economic impacts, generating uncertainty in international trade and logistics." According to the WTO, global growth this year will be less than 1%, in contrast to the 3,5% recorded last year.

Flavia Figueredo He described the current international trade landscape as complex, changing, and full of uncertainty, defining it as a "moving target." He emphasized the importance of upholding the fundamental principles of the multilateral system, such as faith in the law to ensure coexistence, citing jurist Eduardo Couture. However, he warned that today, "the power of the fittest is not only brutality, but also the agonizing uncertainty" that affects the stability of the system.

Figueredo analyzed the global context marked by armed conflicts (Israel, Iran, Gaza, Russia-Ukraine), the post-pandemic, and the geopolitical dispute between China and the United States, where international treaties have become instruments for the consolidation of poles of power, beyond mere trade. In this context, he questioned the recent protectionist measures of the United States, which, although seeking to reduce the trade deficit and reactivate its economy, "violate principles such as transparency, good faith, and legal certainty," generating "great legal uncertainty" with high tariffs that function as instruments of political pressure. He referred to the structural crisis of the World Trade Organization (WTO), whose dispute settlement system is paralyzed by the lack of consensus on appointing the members of the appellate body. He emphasized that this crisis is not new, but has deepened due to the accumulation of exceptions and regional agreements that undermine the most-favored-nation clause and the effectiveness of the multilateral system. In this context, trade retaliation has become a common tool for enforcing decisions, adding uncertainty and tension to global trade.

Finally, Figueredo emphasized that the solution does not lie in discarding multilateral agreements, but in respecting and complying with them "in good faith and with legal certainty." He quoted Nelson Mandela to underscore the need for a more effective regulatory framework that guarantees fair and balanced trade, and called on powerful economies to stop applying unilateral measures while developing countries negotiate their specific needs within that framework. Rebuilding a strong multilateral system, according to Figueredo, depends on political will and prudence in the application of international rules.

El Dr. Hector Juarez Allende continued the thread of the story to address the issue of The powers of the Executive Branches in matters of import tariffs. He conducted a comparative analysis of international systems—the United States, the European Union, MERCOSUR, and others—with the goal of evaluating "which is the best system and weighing the risks of granting broad powers to the executive branch without adequate oversight mechanisms." He defined tariffs not only as a tax, but as an "instrument of economic policy," with "fiscal, regulatory, and geopolitical" functions, illustrating with recent examples from the U.S., such as tariffs applied within the framework of policies against fentanyl, irregular immigration, and measures of (political) pressure on Brazil.

In relation to VOS Selections v. case United States, where various companies and state governments - Oregon, Arizona, Colorado, among many others - are suing the National Government, He explained that President Donald Trump, without any prior market research, imposed tariffs under the IEEPA (International Emergency Economic Powers Act), divided into two categories: “Traffic Tariffs” and “Global and Retaliatory Tariffs.” He emphasized that the United States Court of International Trade (CIT)) declared the tariffs invalid and void, considering that they exceeded presidential authority, that they did not meet the requirement of “dealing with an unusual and extraordinary threat,” that there was no “direct link” between the tariffs and the fight against drug trafficking, and that the “leverage” argument to induce changes was not sufficient. The appeal filed by the National Government before the United States Court of Appeals for the Federal Circuit (CAFC) It was granted without suspensive effect - Trump's tariffs remain in effect - and is pending resolution. The complete document is attached for download. (CIT Ruling – VOS Selections, Inc. v. United States)

Dr. Juárez also referred to cases where national constitutions directly grant exclusive powers to the executive branch to determine tariffs, mentioning Ecuador and Colombia as examples. He then addressed supranational models, such as that of the European Union, where the European Parliament and the Council establish the common tariff with direct and uniform application, and the MERCOSUR regime, which has a Common External Tariff and national exceptions. He highlighted the "double delegation" existing in Argentina—under Article 664 of the Customs Code and Article 5 of Law 22.792, which delegate these powers to the executive branch, and Article 1 of Decree 2.752/91, which subdelegates these powers to the ministers for negotiations within the bloc—and noted that MERCOSUR's supranational nature is "restricted" because it is an intergovernmental integration process. He compared these models to the US system, which features "broad legal delegation, strategic use, and contentiousness." He pointed out risks associated with economic presidentialism, such as discretion and tension with Congress, and emphasized the importance of judicial, legislative, and international checks and balances.

He concluded his presentation with a reflection on the need to strike a balance between effectiveness and legality in the exercise of tariff authority. He emphasized the urgency of reactivating the WTO Appellate Body, whose paralysis limits the effective resolution of trade disputes. He mentioned that, according to various claims submitted within the WTO framework, some provisions such as Article I of GATT 1994 (Most Favored Nation Clause), Article II of GATT (obligation to respect bound tariffs), and the Agreement on Safeguards (SGA) had been violated by the United States. He stressed the importance of promoting control mechanisms for both former before , the ex post, especially in a global context marked by trade wars, reindustrialization processes and the search for strategic sovereignty.

In turn, the Dr. Andres Rohde Ponce He took a critical stance against the overabundance of principles in customs law, instead advocating the inclusion of specific operative rules: "My colleagues began by talking about principles... and I don't like principles. As a jurist, I'm not a big fan of them: there's no point in including the principle of speed in the law if the procedures drag on for years. I prefer that the legal system contemplate specific operative rules, that is, that instead of a principle of speed, precise limitation periods be established. If customs does not act within the period determined by the legislator, the procedure expires and is extinguished."

He acknowledged that some principles, when they become standard, can be useful—such as the pacta sunt servanda—but warned that many customs codes are "born old" and their first articles are "full of principles, even of dubious reputation."

"For example, the principle of trade facilitation... someone explain to me what that means. Or the principle of effectiveness, which is not the same as efficiency."

Rohde Ponce reviewed the principles that underpin the WTO—liberalization, redistribution, reciprocity, and dispute settlement—and noted that, although they have been transformed into obligations, they have been surrounded by numerous exceptions.

He analyzed the United States' shift toward bilateral agreements, driven by Donald Trump, and highlighted the impact of regional blocs, noting that more than 80% of global trade is conducted within them, although with differences: ASEAN (including China) exceeds 70%, the European Union 60%, and NAFTA barely 30%.

"The United States feels excluded by these blocs: 'It's great that the EU is here, but it leaves me out; it's great that Mercosur is here, but it leaves me out.' Mexico understood this in 2000 and signed free trade agreements not to export more, but to import more and secure supplies that would fuel its economic relationship with the U.S.

He also linked trade and investment as inseparable drivers: "Investment and trade make a happy marriage: investment demands protection, and trade demands freedom. If there isn't enough domestic capital, we must attract foreign investment... and to do that, we must open trade."

In this context, he emphasized that the agreement between Mexico and the U.S. will work well, differentiating between automobiles and other products. For the latter, if the rule of origin is met, the 0% tariff remains in place. Most rules of origin are flexible, allowing minimal changes in inputs, while some require a minimum regional content of 50%.

Mexico, however, established a complementary tax in Article 2.5 for non-regional inputs used in products exported to the U.S., although its audit is still pending.

Regarding automobiles, they must comply with a 75% rule of origin to enter tariff-free, but a 25% tax is levied on non-regional inputs. If they do not comply, a 25% tariff is applied to prevent triangulations, in addition to a 30% security tax, the implementation of which has been postponed. Regarding non-tariff barriers, the United States has published a document outlining the topics it intends to negotiate bilaterally, including telecommunications, labor issues, and other disciplines under the umbrella of non-tariff measures.

This context marks a return to bilateralism, without necessarily meaning a break with multilateralism.

Finally, he emphasized that the US and Mexico agenda is not limited to trade or tariff issues, but is deeply shaped by challenges such as organized crime, migration, and security, which are the true sources of tension in the relationship between the two countries.

And he concluded: "As hasn't happened in the last 50 years, today we are in a bilateralism, and the United States is setting the agenda for global trade."

Closing words

The closing ceremony of the conference was led by Eduardo Vázquez, Vice President of the AAEF, and of course by Gustavo Zunino, Vice President of the Scientific Committee.

El Dr. Zunino He structured his presentation around three fundamental axes, inspired by the integrative spirit of the Conference as an academic beacon in which all voices were present. First, he echoed the opinion of the Deputy Director of Legal and Technical Affairs of Customs, who highlighted how these meetings allow the institution to update itself alongside the private sector, providing a broad and enriching perspective. Second, he underscored the active participation of young people, citing Dr. Pablo Labandera's observation on how their inclusion guarantees the continuity of academic activities. Finally, he referred to the principle of the common good, echoing a statement by Dr. Miguel Licht, expressed at the opening, on the relevance of this value as the foundation of customs law.

In that same line, the Dr. Vázquez He reaffirmed the spirit of the AAEF, expressing his gratitude to the directors, the Scientific Committee, and the Executive Committee, as well as to the coordinators, national and international speakers, and those who support the committees throughout the year with their selfless commitment. He emphasized that the debates have an international reach and that the sessions are valuable because they generate solutions that benefit the professionals involved and, ultimately, the country.

(I.e.Recommendations from the International Conference on Customs Law, presented by Dr. Lorena Bartomioli and Dr. Fernando Schettini

"The purpose of the recommendations is not to modify the content of the Conference, but rather to emphasize those priority points on which we consider it essential to move forward," said Dr. Lorena Bartomioli, accompanied by Dr. Schiettini, members of the AAEF Executive Committee.

"Our mission is to focus attention on these aspects to achieve effective solutions." Namely:

1) Reaffirm the principle of legality as a structural basisIt is emphasized that the legislature cannot delegate to the Executive Branch the determination of the parameters or reference values for the tax base without clear guidelines and limits, especially when establishing theoretical bases or official prices. Congress must safeguard the principle of tax legality, since all tax burdens, including customs value adjustments, must be based on rules with legal hierarchy. Replacing the GATT customs valuation regime with external guidelines without express legislative approval is unacceptable.

2) Principle of tax neutralityIt is recommended to maintain neutrality regarding theoretical bases for consumption taxes, including customs duties, seeking to minimize competitive distortions. It is essential to carefully evaluate the impact of specific or theoretical bases unrelated to actual transactions, to avoid favoring certain actors or products to the detriment of others, thereby affecting domestic and international competition.

3) Digitalization and customs processesThe elimination of in-person procedures and dematerialization should not reduce international trade operators' ability to review, challenge, or defend themselves. Tools such as the digital file, the stock report, and the comprehensive customs declaration should include regulatory validation mechanisms, the right to reply, proof of deadlines, and accessible means of appeal. Comprehensive digitalization that respects legal principles such as legality, the validity of consent, electronic notification, the right to evidence, and systemic accountability is encouraged.

4) Due process guarantees.It is proposed to reform the substantive nature of the request for a hearing, considering it an essential guarantee of due process. The omission of the procedure provided for in Article 1101 of the Customs Code cannot be viewed as a mere formality. It is also recommended to shorten the statute of limitations, establishing that suspension or interruption occurs upon notification of the act, not upon the administrative act itself.

5) Strengthening the suspensive nature of appealsMechanisms that recognize the full effectiveness of the suspensive nature of the hearing request must be strengthened, especially regarding the time limits for filing appeals before the National Tax Court.

6) Implementation of a single electronic system.The proposal is to integrate the current electronic systems (SIME, SIMEA, SICNEA, GDE, VUCE, and SUGA) into a single electronic customs filing system that will permanently replace paper in administrative and contentious procedures, guaranteeing permanent access to proceedings, document traceability, transparency, proper application of the positive silence rule, and compliance with constitutional guarantees and the right to defense.

7) Update of amounts for access to administrative justiceIt is recommended that the minimum amounts for accessing the National Tax Court be reviewed and updated, especially those provided for in Article 1025 of the Customs Code, adapting them to the current economic context to ensure effective judicial protection against administrative acts of significant economic significance.

8) Appeal system for delay.It is proposed to reform this regime, establishing that the appeal procedure for administrative delay is activated not only by the late issuance of the resolution, but also by delays in processing the procedure.

9) Compliance with due process and trade facilitationFinally, due process is fully respected in customs procedures through a unified, transparent, and efficient system that ensures compliance with legal deadlines, effective participation of the governed party, proper application of administrative silence, and the adoption of international standards in trade facilitation.

The AAEF will compile and classify the corresponding speeches, presentations, and reports for publication. In the meantime, and given the success and high turnout of the 2025 International Customs Law Conference, this summary prepared by Aduana News It summarizes the various topics addressed, with the expectation that it will constitute a contribution of interest to the community.

Aduana News foi o primeiro jornal aduaneiro da Argentina a lançar sua versão digital. Com mais de 20 anos de trajetória, suas publicações e iniciativas têm como objetivo oferecer o conhecimento mais relevante sobre temas aduaneiros, contribuindo para a promoção do comércio seguro e da facilitação do comércio na região.