🟦1. From the novel instrument to fundamental concepts

This topic serves the dual purpose of being a current and relevant issue, given that administrative and judicial challenges have already been raised regarding it; and also because, coinciding with the publication date of this column, a new instrument will be approved within the framework of the World Customs Organization, which sheds light on the topic.

Certainly, these days – from Thursday 26 June to Saturday 28 June 2025 – the World Customs Organization Council Meeting (145th and 146th Council Sessions) is taking place in Brussels, which has within its broad agenda (1) the approval of Advisory Opinion 26.1 of the Technical Committee on Customs Valuation, referring to the “Treatment applicable to transactions agreed upon in cryptocurrencies not recognized as legal tender”.

In this regard, the Technical Committee on Customs Valuation (CTVA) at its 59th Session held in Brussels on 14-18 October 2024, adopted its one hundred and one technical instrument: Advisory Opinion 26.1: “TREATMENT APPLICABLE TO TRANSACTIONS AGREED IN CRYPTOCURRENCIES NOT RECOGNISED AS LEGAL TENDER”(3).

As its title indicates, the Opinion refers to “cryptocurrencies,” and particularly to cases where the transaction is agreed upon in “cryptocurrencies.”

While the opinion expressed by the Customs Valuation Technical Committee answers a specific question, it resolves several hypotheses and allows for solutions to others not specifically addressed in the text.

All of this gives us the opportunity to establish some distinctions in the treatment applicable to cryptocurrencies in terms of customs value, based on inputs that should be understood as already understood, and which may also be useful to revisit.

🟦2. Cryptocurrencies and customs valuation

Cryptocurrencies are a form of digital money that uses blockchain technology to ensure secure and decentralized transactions.

Unlike money issued by states, or unions of states, cryptocurrencies are not controlled by a central government or entity, but operate through decentralized networks that employ advanced cryptography to secure their operations.

There are several cryptocurrencies worldwide: Bitcoin (which was the first and currently the largest cryptocurrency by market capitalization); Bitcoin Cash; Stellar; Ethereum; Solana; Litecoin; EOS; NEO; among others.

Cryptoassets, on the other hand, are a broader term that encompasses not only cryptocurrencies but also other digital assets based on blockchain technology. Cryptoassets are a representation of value or rights, whether or not they are cryptographically secured. These include tokens, smart contracts, and other digital instruments that can represent values, rights, or property.

While cryptocurrencies are primarily used as a medium of exchange or store of value, cryptoassets can have additional functions, such as representing company shares, physical assets, or even access to specific services within blockchain platforms.

In another sense, all cryptocurrencies are cryptoassets, but not all cryptoassets are cryptocurrencies. The relationship between the two lies in their shared origins within the blockchain ecosystem, with cryptocurrencies being a specific category within this broader universe.

Thus, since cryptocurrencies are a medium of exchange, they can be used to pay for the delivery of goods and services. Therefore, cryptocurrencies can be used to purchase imported goods.

Considering its function and the sustained growth in the use of cryptocurrencies, the Technical Committee on Customs Valuation noted the need to analyze and issue an opinion to determine the customs valuation treatment for the purchase and sale of goods to be imported using cryptocurrencies.

🟦3.On the structure and content of Advisory Opinion 26.1

Advisory Opinion 26.1 of the Technical Committee on Customs Valuation contains nine paragraphs.

The first three numerals conceptualize and differentiate what are “digital assets,” “crypto assets,” and “cryptocurrencies.”

By considering "cryptocurrencies" as a type of cryptoasset designed as a form of "money" outside of central banking systems to be used to settle payment obligations, the Technical Committee on Customs Valuation highlights the problems that may arise in customs valuation matters, as expressed in Advisory Opinion 26.1.

In this sense, in numeral 4 the question is formulated: How should the customs value be determined when goods are presented for import following a purchase agreed upon in cryptocurrencies not recognized as legal tender in the importing country?

The question is answered in paragraphs 6 to 9, as announced in paragraph 5. Thus, paragraph 6 establishes the conceptual and regulatory framework necessary for the answer, by referring to the definition in article 1.1 of the Value Agreement (4), and the conditions for the application of the transaction value, recalling that the referred method requires the existence of a price for its application, and that in accordance with Article 9 (5), said price must be expressed in the currency of the importing country or be capable of being converted into the currency of the importing country.

Now, the initial question posed by the Customs Valuation Technical Committee, which is answered in sections 6 to 9, assumes a purchase agreed upon in cryptocurrencies not recognized as legal tender in the importing country.

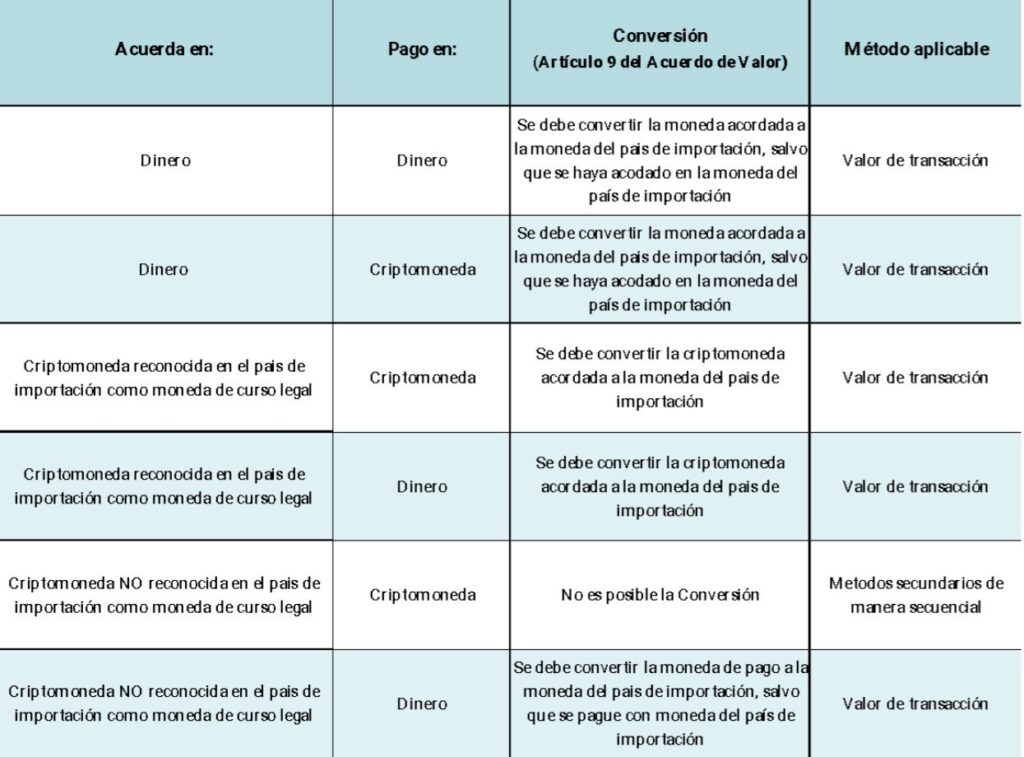

This hypothesis, where the purchase was agreed in cryptocurrency, may have two alternatives in relation to its payment (cancellation):

a) that is paid in cryptocurrency; or

b)to be paid in legal tender (which could also be the currency of the importing country).

This distinction between how the agreed-upon cryptocurrency purchase is settled is relevant for valuation purposes, as it will determine whether the transaction value can be applied or not.

Thus, paragraph 7 of Advisory Opinion 26.1 determines that for Members that do not recognize cryptocurrencies as legal tender, the price in transactions agreed in cryptocurrencies is not convertible in accordance with Article 9. Therefore, there is no price for the purposes of applying the transaction value method. It adds that, as a result, the customs value cannot be determined in accordance with Article 1, but must be established by applying one of the other methods established in the Agreement, sequentially.

While paragraph 8 determines that, notwithstanding what is referred to in points 6 and 7, it is possible for the sales contract to establish the price in cryptocurrency, but for the transaction to be finally settled (that is, paid) by the buyer in a currency recognized as legal tender, as agreed between the contracting parties (buyer-seller).

In such a case, the Technical Committee on Customs Valuation establishes that the customs value could be determined on the basis of Article 1 and, if necessary, converted into the currency of the importing country in accordance with Article 9. To be clearer, in circumstances where the purchase is agreed in cryptocurrency and settled in a currency recognized as legal tender, the customs value could be determined on the basis of Article 1 (when the payment currency is the currency of the importing country, such as Uruguayan pesos in Uruguay), without the need for conversion; and, if necessary – because the payment currency is not the currency of the importing country (eg: Uruguayan peso in Uruguay) –, converted into the currency of the importing country in accordance with Article 9 (eg: convert to Uruguayan pesos in Uruguay).

In addition, Section 8 establishes that Article 17 of the Agreement emphasizes the right of Customs Administrations to verify the truthfulness or accuracy of any information, document, or declaration submitted for customs valuation purposes. We understand that invoking Article 17 of the Valuation Agreement is intended to be clarifying (and perhaps "reassuring"), since its application is already a matter of principle.

It is interesting to note that in these cases, the Customs Administration of the importing country should be able to ensure that the price paid in cash is equivalent to the obligation agreed in cryptocurrency at the time of cancellation. However, while there is an advantage in these situations, as it must determine the equivalence, this does not differ in terms of the objective, which will be to verify that the total amount paid corresponds to the contractually agreed obligation, which is what the Customs Administration must verify in any contract agreed and paid in cash.

Finally, paragraph 9 determines that the analysis contained in paragraphs 6 to 8 is not relevant to those Members that do recognize cryptocurrency as legal tender.

🟦4. The possibility or not of conversion of Article 9 of the Value Agreement as a determining factor for the applicability of the transaction value

A quick reading of this novel instrument might lead one to understand that the problem with cryptocurrencies is their disregard for currency, which would mean that there is no price and, consequently, that the first valuation method of the Value Agreement (transaction value) could not be applied. But this is not the point.

I understand that, in relation to their status as money, the definition of cryptocurrencies established in Advisory Opinion 26.1 by the Technical Committee on Customs Valuation recognizes such status, since it establishes that cryptocurrencies are a type of cryptoasset designed as a form of money outside of central banking systems to be used for the settlement of payment obligations, among other purposes.

But if you look closely, the problem isn't the disregard for merchandise purchase agreements set in cryptocurrencies not recognized as legal tender in the importing country because they are not considered "money," but rather the impossibility of converting them into the currency of the importing country.

Note that if the currency agreed upon in the purchase and sale of imported goods is that of the importing country, the price set in that currency will be accepted, and obviously, no conversion will be required. However, what normally happens (due to, among other reasons, the widespread use of the dollar and the euro in international trade) is that the currency agreed upon in the contract must be converted into the currency of the importing country.

Now, when we are dealing with a purchase agreed upon in cryptocurrency, which is not recognized as legal tender in the importing country, it is evident that the cryptocurrency will not be the currency of the importing country, and therefore, conversion to the same currency (the currency of the importing country) will be required. However, since the cryptocurrency is not recognized as legal tender in the importing country, it cannot be converted into the currency of the importing country, according to Article 9 of the Securities and Exchange Agreement.

Substantially, the cryptocurrency agreed upon in the purchase of imported goods that is not recognized in the country of import as legal tender in the country of import is inconvertible (or non-convertible) into the currency of the country of import (Article 9 of the Securities Agreement).

However, if the original obligation agreed upon in cryptocurrency is ultimately settled with currency recognized in the importing country prior to import, it would be possible to apply the transaction value method, but not based on the amount agreed upon, but rather on the amount paid.

Therefore, it is important to differentiate between the cases in which we are dealing with purchases and sales that were agreed upon in cryptocurrencies, but it is essential to know how they were settled.

Thus, the fact that it was agreed in cryptocurrencies is not sufficient to rule out the application of the transaction value, since, if this circumstance still occurred, but the obligation originally agreed in cryptocurrencies is paid (settled) with a legal tender currency, by agreement between the parties involved in the contract, the customs value may be determined in accordance with Article 1 of the Value Agreement, since it will be susceptible to being converted to the currency of the importing country, unless it was paid with the currency of the importing country and the conversion would not be necessary.

However, if the obligation is agreed upon in cryptocurrency and is paid in cryptocurrency, as mentioned above, the transaction value method cannot be applied, and the appropriate secondary method must be applied, in sequential order. Similarly, if the obligation agreed upon in cryptocurrency is to be paid through any other non-monetary consideration.

🟦5. A basic distinction: Agreeing is not the same as paying.

Now, let me step back a bit from Advisory Opinion 26.1 and review a point that is clear in this instrument, which is the difference between agreeing (covenanting) and paying.

In relation to a sale, agreeing on the price, setting the price, arranging the price or agreeing on the price – which are all equivalent expressions –, turns out to be the manifest expression of the will of the parties, which produces legal effects, by which the price of the thing being sold is determined, and which the buyer is obliged to pay.

While paying refers to the action of delivering a sum of money or another form of compliance as payment for a debt or agreement, being the natural means of extinguishing the obligation incurred.

However, there is a substantial difference for the purposes of valuation and the possibility of applying Article 1 of the Value Agreement (Transaction Value Method) between agreeing (fixing) the price of the goods sold for import (and consequently expressing it in the corresponding documentation, that is, in the Commercial Invoice), and paying the price duly fixed.

In this regard, what is relevant for the purposes of customs valuation of imported goods is how the consideration for the imported goods is agreed upon in the transaction, and not how the agreed obligation is paid. This is the case, except in the case where, as we saw, the buyer is paying an obligation originally agreed upon in a cryptocurrency not recognized by the importing country as legal tender, as agreed between the contracting parties (buyer and seller).

🟦6.Of the various assumptions and their solutions

From the foregoing, it follows that the assumptions of Advisory Opinion 26.1 focus on cryptocurrencies. They differentiate, on the one hand, between the assumptions contemplated in paragraphs 6 to 8, where a contract of sale for goods to be imported is agreed upon in cryptocurrencies not recognized by the importing country as legal tender; and, on the other hand, the assumptions contemplated in paragraph 9, which, by exclusion, determines that the analysis contained in paragraphs 6 to 8 is not relevant to those Members that do recognize cryptocurrency as legal tender, in which case it is treated in the same way as money.

However, there is a possible scenario where cryptocurrency could be used, and which is not addressed by Advisory Opinion 26.1, which is the case where the agreement is made in money (in the currency of the importing country or any other currency that is recognized by the importing country as legal tender) but the original obligation is settled with cryptocurrency.

In this case, the distinction between agreeing and paying, to which we referred previously, is useful, as is the relevance that the price set for the settlement (payment) of the originally agreed debt has in customs valuation matters.

Thus, for the purposes of the assessment, the way in which the obligation fixed in money is settled has no influence, except in the case seen (contemplated in section 8 of Advisory Opinion 26.1).

This was already stated by LASCANO in his 2007 work, when referring to the “instrumentation of payment”:

“The method of payment is also irrelevant, as is whether part of the payment is made in cash and the remainder is delivered through the delivery of goods and services. Furthermore, the importer's consideration may consist of the delivery of goods and services for a value equivalent to that of the merchandise., provided that the parties have agreed on a price for the transaction, as we have already seen in the cases of exchange.”(6)

Therefore, the solution is simple: it makes no difference how a monetary obligation is settled for the purposes of applying the transaction value method.

Finally, in the following table I have determined the different assumptions that may occur, and the method that would be applicable, provided that the conditions established in Article 1.1(a) to (d) of the Value Agreement are met.

🟦7. Some closing clarifications

Advisory Opinion 26.1 accepts that cryptocurrencies are a type of cryptoasset designed as a form of money outside of central banking systems to be used for the settlement of payment obligations, among other purposes.

Notwithstanding this, the aforementioned instrument determines the impossibility of applying the transaction value to imports of goods agreed upon in cryptocurrencies not recognized by the importing country as legal tender, given their impossibility of being converted into the currency of the importing country.

An exception is when in such cases the obligation in question is settled with the currency of the importing country or currency recognized as legal tender by the importing country, as this allows for the application of Article 9 of the Securities Agreement.

To determine the possibility of applying the transaction value, only the agreed currency must be considered, and not the form of payment, except for the case referred to above.

It is irrelevant for the purposes of applying the transaction value whether an obligation agreed in money is settled in cryptocurrency.

I understand that Advisory Opinion 26.1 will shed sufficient light on how cryptocurrencies should be treated.

We will know soon.

2.Technical Committee on Customs Valuation (TCCV)

3. The text has not been officially published as it has not yet been approved by the WCO Council.

4. Agreement on the Implementation of Article VII of the General Agreement on Tariffs and Trade 1994.

5.Article 9

1. In cases where the conversion of a currency is necessary to determine the customs value, the rate of exchange to be used shall be the one duly published by the competent authorities of the importing country concerned and shall reflect as accurately as possible, for each period covered by such publication, the current value of that currency in commercial transactions expressed in the currency of the importing country.

2. The applicable exchange rate shall be the one in force at the time of export or import, as stipulated by each Member.”

6.LASCANO, Julio Carlos. The Customs Value of Imported Goods. Osmar D. Buyatti. Buenos Aires. 2007. Pages 127 and 128

Doctor of Law and Social Sciences, Faculty of Law, University of the Republic (Uruguay). Adjunct Professor (UR), in charge of the undergraduate courses ofCustoms law(Law), and ofLegal Regime of Foreign Trade II: Customs Law(Bachelor of International Relations); and the SeminarCustoms infringement law, at the Faculty of Law, University of the Republic (Uruguay).

As a lecturer in charge, he has taught various courses in his specialty at the Graduate School, Faculty of Law, University of the Republic (Uruguay).

General Coordinator and speaker at the Academic Conferences on Customs Law (2014–2025). Speaker at multiple national and international events and author of several articles on the subject.

President of the Latin American Academy of Customs Law. Member of the Institute of Public Finance (Udelar) and the Argentine Association of Fiscal Studies. Partner at Varela – Customs Law Firm (Montevideo, Uruguay).

Email:[email protected]